What is Lumber Financing and How Does it Work?

Lumber financing is a vital aspect of the wood industry. As the demand for timber increases, securing financial resources becomes essential. According to the U.S. Forest Service, the U.S. timber industry is valued at over $200 billion. This highlights the industry's economic importance.

Many businesses rely on lumber financing for purchasing raw materials. It supports mills, wholesalers, and retailers in maintaining stock levels. However, accessing these financial resources can present challenges. Interest rates may fluctuate, affecting overall project costs. Recent reports show that nearly 30% of small businesses face difficulties in securing funding.

Evolving market conditions require constant adaptation in lumber financing strategies. Borrowers often need to assess the stability of their cash flows. They must also consider the long-term implications of their financing choices. As competition intensifies, identifying the right financial partners becomes crucial. In this context, an understanding of lumber financing is more important than ever.

Understanding Lumber Financing: An Overview

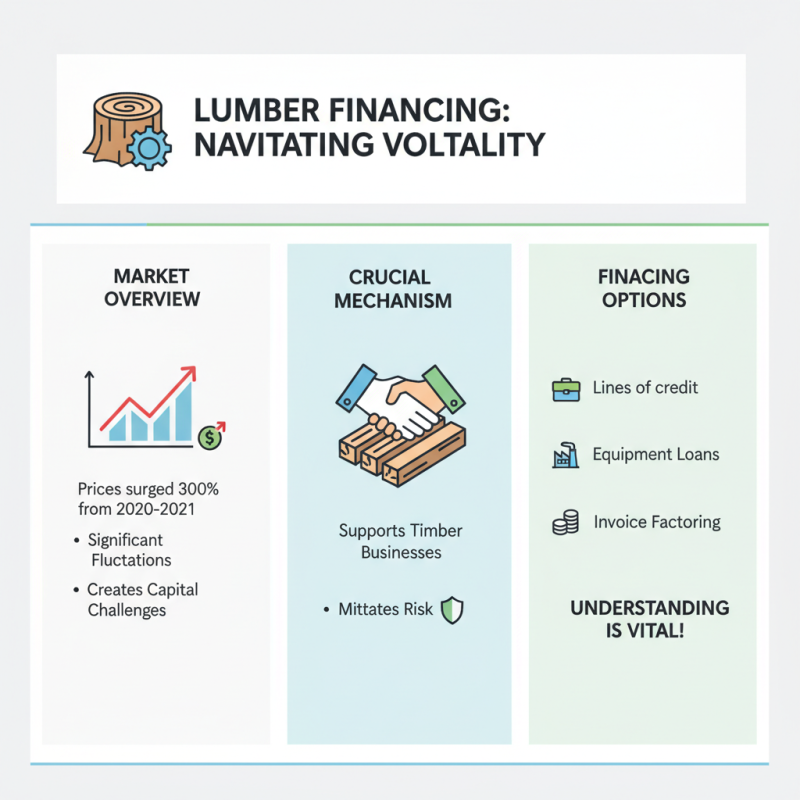

Lumber financing serves as a crucial mechanism for businesses in the timber industry. The lumber market has seen significant fluctuations. According to recent data, lumber prices surged 300% from 2020 to 2021. Such volatility creates challenges for companies that require capital. Understanding the specific financing options is vital for these enterprises.

Lumber financing can involve various solutions like short-term loans and inventory financing. These methods enable businesses to manage cash flow effectively. For instance, a report from the National Association of Home Builders highlighted that nearly 80% of builders faced material scarcity in 2022. This scarcity created pressure to secure reliable financing sources.

However, the intricacies of lumber financing are not always clear. Many companies struggle to find favorable terms. High-interest rates can deter businesses from pursuing necessary funding. The lumber sector, though essential, often experiences uncertainty. As firms navigate these challenges, understanding the landscape is crucial for sustainable growth. Making informed decisions can significantly affect their financial health and stability.

The Process of Obtaining Lumber Financing

Obtaining lumber financing involves several steps that can significantly impact project success. The borrower usually starts by assessing their financial needs. According to a report from the National Association of Home Builders, nearly 70% of lumber-related projects require some form of financing. This statistic highlights the importance of securing adequate funds.

Next, it's essential to explore various financing options available in the market. Borrowers can choose from traditional banks, credit unions, or specialized lenders. Research shows that interest rates can vary significantly, impacting the overall project budget. A 2023 survey found that rates for lumber financing could range from 4% to 10%, depending on the lender and the borrower’s credit profile.

After selecting a lender, the application process begins. This typically involves providing financial documents, project details, and collateral information. Incomplete applications can stall the process, delaying critical timelines. It’s crucial to ensure all required documents are prepared in advance. Many borrowers overlook this, which can lead to complications or rejected applications. Resilience and organization are key to navigating this intricate financing landscape effectively.

Lumber Financing Overview

This bar chart represents the financing amounts in thousands of dollars across the four quarters of 2023, illustrating the trend in lumber financing over the year. As seen, the values show an increasing trend, indicating potentially growing demand and investment in lumber financing.

Key Factors Influencing Lumber Financing Rates

Lumber financing is vital for many businesses in the construction and woodworking industries. The rates for lumber financing can vary greatly. Several key factors influence these rates, including market demand, credit risk, and seasonal fluctuations.

Market demand plays a significant role. When demand for lumber surges, financing rates may increase. This happens because lenders recognize increased risk during high-demand periods. Similarly, credit scores of borrowers can also affect the rates. Higher credit scores typically lead to lower financing costs. On the other hand, a poor credit history might raise the rates unexpectedly.

Tips for securing better financing rates include improving your credit score. Review your credit report for errors and dispute any inaccuracies. Furthermore, consider timing your financing. Rates tend to be lower during off-peak seasons. Lastly, keep a close watch on lumber market trends. Understanding these fluctuations can optimize your financing decisions, yet many overlook this important step. Awareness is key for better pricing.

Benefits and Risks of Lumber Financing for Businesses

Lumber financing helps businesses secure funds for wood products. This type of financing can be beneficial, but it also carries risks. Companies might face financial strain if the market fluctuates. They need to understand the implications of borrowing against lumber inventory.

Benefits of lumber financing include improved cash flow. Businesses can invest in necessary equipment or manage operational costs. Access to quick capital can also help maintain inventory levels. This agility can benefit companies during high-demand seasons.

However, relying heavily on financing has its drawbacks. Increased debt can lead to financial instability. Market price drops may leave a business with depreciated assets. It’s essential for companies to weigh these risks before proceeding.

Tips: Assess your inventory carefully. Know how much you can borrow without overextending. Consider using a diverse range of financing options. This helps mitigate potential losses from unexpected market changes.

What is Lumber Financing and How Does it Work? - Benefits and Risks of Lumber Financing for Businesses

| Dimension |

Details |

| Definition |

Lumber financing refers to financial services provided to businesses within the lumber industry to support their operational and growth needs. |

| Benefits |

Provides necessary cash flow, helps manage seasonal fluctuations, and supports expansion plans. |

| Common Financing Options |

Lines of credit, term loans, invoice financing, and equipment leasing. |

| Risks |

Potential for increased debt, fluctuating lumber prices, and economic downturn impacts. |

| Ideal For |

Lumber manufacturers, wholesalers, retailers, and related businesses in need of working capital. |

| Considerations |

Business creditworthiness, interest rates, repayment terms, and lumber industry trends. |